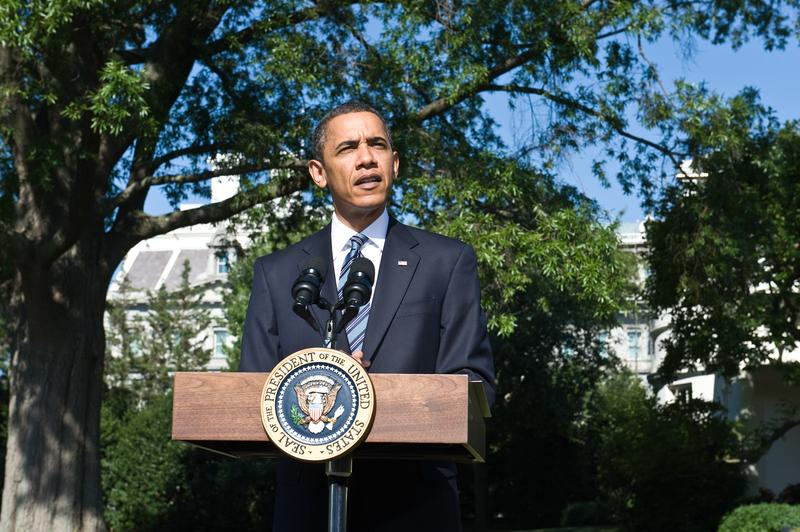

Published by WQXR News G-20 Leaders Vow to Reduce Debt President Barack Obama delivers a statement on financial reform before deparrting the G8 and G20 summits in Toronto at the White House in Washington,DC on June 25, 2010. i Post a Comment